Long: P10 Holdings (PX: NYSE)

Current Price: $11.80 (Jan 30, 2022)

Share Count Diluted: 125 mm, Market Cap: 1.5 billion, EV = 1.84 billion

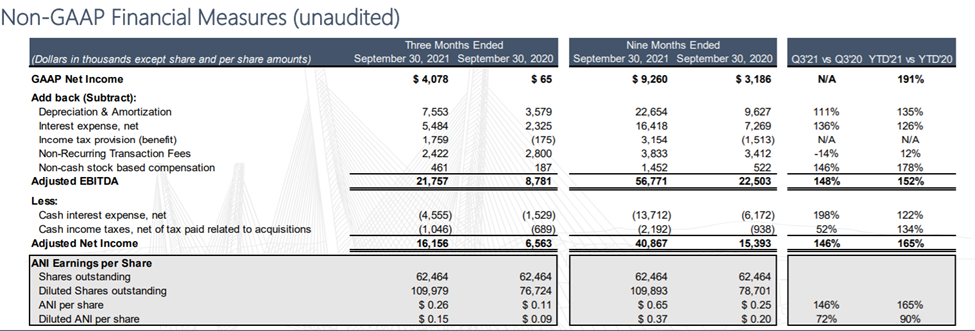

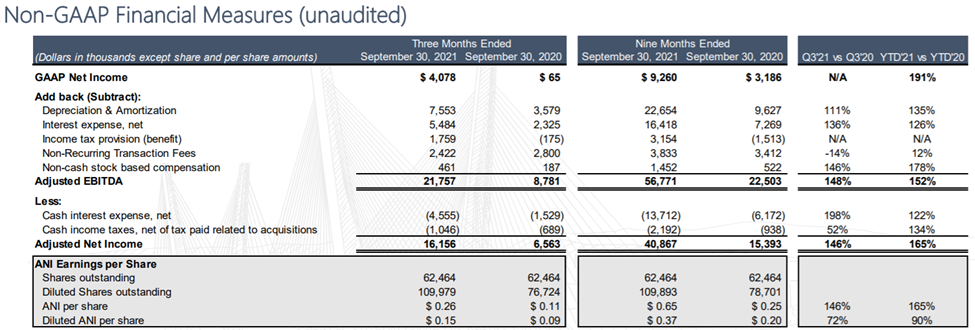

2022 est. EBITDA = 100 mm, EV/EBITDA = 18.4

Opportunity

P10 Holdings is a multi-asset class, private markets solution provider in the lower/middle market alternative asset space. Its business model delivers high margin revenue and highly predictable returns from the ownership of the management and advisory fees of the fee-paying assets under management (FPAUM). With just a 1.5 billion market cap, strong organic growth, an unique and attractive value proposition for the companies it acquires, PX should be capable of 25% plus annual increases in FPAUM, revenue and free cash flow.

P10 Introduction

For its customers, P10 Holding offers its clients differentiated access to a broad set of solutions and specialized investment vehicles primarily in the lower/middle market alternative asset space.

For its shareholders, P10 Holdings is a company with an attractive business model that generates extremely predictable, recurring, high margin fixed management fees earned on the committed capital in long-term contractually locked up funds.

Our revenue is composed almost entirely of recurring management and advisory fees, with the vast majority of fees earned on committed capital that is typically subject to ten to fifteen year lock up agreements. We have an attractive business model that is underpinned by highly recurring, diversified management and advisory fee revenues, and strong free cash flow. The nature of our solutions and the integral role that our solutions play in our investors’ investment decisions have translated into high revenue visibility and investor retention.

From the 2021 Prospectus

Unlike financial holding companies that purchases an equity stake in an asset manager’s general partner, P10 only purchases the management fee of the solution provider it acquires for cash and stock and leaves the performance fee and carried interest of the acquired fund with the original management team. The acquired company becomes a variable interest entity (VIE) under P10 Holdings. This structure ensures the acquired managers continue focusing on performance and can continue raising new assets off their track record.

We specifically aim to eliminate perceived challenges facing many publicly traded alternative asset management firms, (i) earnings volatility due to lumpiness of carried interest, (ii) tax complexities from the ownership of management and advisory fees and carried interest in publicly traded partnerships and (iii) potential misalignment of interest between investment professionals and the shareholders.“

From the 2021 Prospectus

Established solution providers are incented to sell to P10 because the P10 business model allows the sellers the opportunity to exchange the equity built up in their private partnerships for cash and shares of a diversified public company without losing their ability to earn the performance carry on the current and the future assets they manage and raise. For P10, the same fee split structure ensures the fund’s management team stays fully motivated to outperform.

P10 History and Management

The history of P10 Holdings begins with 210 Capital LLC which Robert Alpert, 56, and Chuck Webb, 40, co-founded in 2017. In addition to P10, 210 Capital owns or controls Crossroads Systems, Elah Holdings, and Globalscape. Alpert and Webb serve in executive roles at all their companies as either CEO, co-CEO, and/or Chair.

Prior to founding 210 Capital, Robert Alpert was the founder and portfolio manager of Atlas Capital Management, LP, a long-short strategy investment adviser from October 1995 to September 2015. Previously, Clark Webb was a Co-Portfolio Manager of the Lafayette Street Fund and a Partner at Select Equity Group, L.P.

In 2017, 210 Capital acquired what became P10 Holdings out of bankruptcy court and through a support agreement made Robert Alpert and Clark Webb co-CEO’s of P10 Holdings with Alpert also serving as Chair. As of June 30, 2021, 208 million of Net Operating Loss (NOL) carry forwards remain available.

At inception, P10 was an empty shell corporation without an operating business. In October 2017, Alpert/Webb’s first P10 acquisition was RCP Advisors, a sponsor of private equity, funds-of-funds, secondary funds, and co-investment funds. Since its founding in 2001, RCP Advisors has raised approximately $7 billion of committed capital and maintains one of the largest internal teams dedicated to North America middle and lower-middle market private equity.

Importantly, P10 only receives the management fees generated from the RCP funds, not the carried interest. We believe that the carried interest provides an alignment between the RCP investment team and its investors. In other words, we want the carried interest to go to the RCP professionals, as it provides those individuals with economic incentives to continue to perform on behalf of investors. The benefit to P10 is twofold: (1) we have an RCP team that remains highly motivated to perform; and (2) the P10 revenues consist almost exclusively of highly predictable and stable management and advisory fees. Moreover, we have an extraordinary team in place with significant capacity to add incremental assets undermanagement (“AUM”). As a result, to the extent we can continue to grow our AUM, thereby growing our management fees, we would anticipate an expanding profit margin and growing earnings for P10. For 2018, we project the RCP business should generate an EBITDA margin in excess of 50% of revenues; and because our management fees are, for the most part, locked up by contract for up to a decade, we believe this profit stream will prove to be stable.

As part of the transaction, RCP principals received 44.17 million shares of P10 common stock, representing approximately 49.5% of our post-acquisition capitalization, making them the largest stockholders of P10, by far. Two RCP partners, Fritz Souder and Jeff Gehl also joined the board of directors of P10. “In addition to the shares of common stock, P10 issued to the RCP principals approximately $117 million in principal amount of non-interest bearing promissory notes (the “Sellers’ Notes”).”

From the 2017 P10 Shareholder letter

The projections in the letter proved out. RCP revenues in 2018 were 32 million with margins of 55%. Additionally, Fritz Souder continues to serve on the P10 board and as Chief Operating Officer of P10 Holdings as well as Managing Partner and President of RCP. Jeff Gehl continues as Head of Marketing and Distribution of P10 Holdings as well as Managing Partner and Vice President of RCP. Jeff Gehl remained on the P10 board until September 2021 when he stepped down to make room for Ewin Poston, managing partner of TrueBridge Capital and Scott Gwilliam from Keystone Capital to join the board.

P10’s 2020 Acquisitions

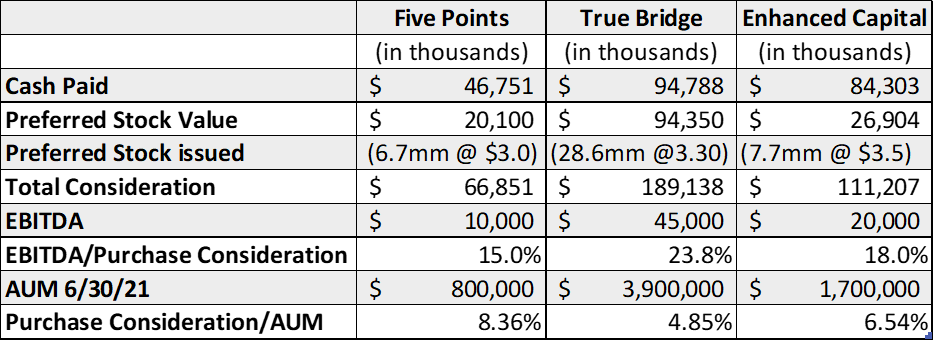

In April 2020, P10 acquired Five Points, a lower middle market alternative investment manager focused on providing both equity and debt capital to private, growth-oriented companies and LP capital to other private equity funds. At acquisition, its strategies focused exclusively on the U.S. lower middle market. Since its founding over two decades ago, Five Points has successfully raised and deployed more than $1.5 billion on behalf of institutional and high net worth clients.

In October 2020, P10 closed on the acquisition of TrueBridge, a leading venture capital investment firm managing more than $3.3 billion in assets. TrueBridge invests in venture and seed/micro-VC funds focused primarily on early-stage IT, as well as directly in select venture and growth stage technology companies.

In December 2020, P10 closed on the acquisition of Enhanced Capital, LLC, an impact investment firm with a two-decade history of deploying capital into socially responsible investment areas including small business lending, renewable energy, and women and minority owned businesses. Since inception, Enhanced has deployed more than $3 billion across its impact verticals.

On September 30, 2021, P10 purchased Bonaccord Capital Partners and Hark Capital from the asset manager abrdn. Unlike their acquisitions of stand-alone companies which include a stock component, this was a cash transaction for 40 million and up to 25.4 million in earnouts. The management teams will transition to P10 and operate from within the P10 Private Equity and Private Credit asset management groupings respectively.

Bonaccord acquires minority equity investments in a diversified portfolio of alternative markets asset managers with a focus on mid-sized managers across private equity, private credit, and real assets. Hark provides loans to mid-life private equity, growth equity, venture, and other funds. P10 expects the transactions to add approximately $900 million in fee paying assets under management.

Price paid for 2020 Acquisitions

Historical Performance Drives Organic Growth

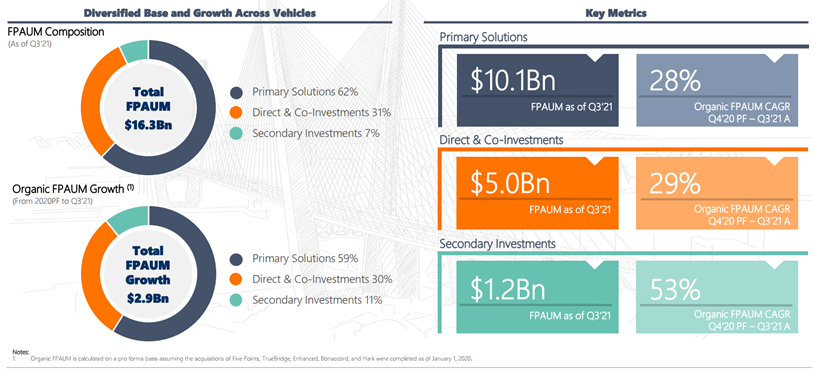

P10’s organic growth is strong and is growing about 30% pro-forma in 2021. Given past performance, the ability of the management teams to raise larger sums for their newest funds in a strong market is not surprising. P10 fund raising benefitted in 2021 from a favorable fund offering calendar, but in 2022, there will be fewer new offerings of existing strategies as not every product is offered every year. Based on the calendar, 2023 and 2024 will have more new offerings than 2022.

P10 FPAUM Growth

P10 Investment Managers Track Records

Growth driven by leveraging relationships in P10’s Private Market ecosystem

The private market ecosystem lends itself to cross-solution sourcing of investors and investments as well as leverage its proprietary database of middle and lower middle market private venture data.

As we expand our offerings, our investors entrust us with additional capital, which strengthens our relationships with our fund managers, drives additional investment opportunities, sources more data, enables portfolio optimization and enhances returns, and in turn attracts new investors. We believe this powerful feedback process will continue to strengthen our position within the private markets ecosystem. In addition, our multi-asset class solutions are highly synergistic, and coupled with our vast network of general partners and portfolio companies, drive cross-solution sourcing opportunities.”

from the 2021 S-1

Growth through Geographic expansion

Second, there are opportunities for cross selling and leveraging networks of investors and investments across the company’s platform especially geographic expansion. At the Annual meeting in July 2021, Alpert/Webb gave the example of introducing the TrueBridge fund to European investors in its network where TrueBridge was previously unknown and raised 700mm in new commitments.

Alternative Assets Market Growth

P10’s middle and lower-middle markets funds that invest in portfolio companies with revenues between $25 and $500 million is an underserved, growing and relationship-oriented market where growing scale generates a self-reinforcing virtuous cycle. This market is too small for firms like BlackRock with trillions in assets to pursue, but it is a long runway for growth for a firm like P10.

Acquisitions

While future acquisitions are a given, their timing will never be predictable. At the Annual Meeting in July 2021, Robert Alpert mentioned that discussions are usually occurring with 6-7 firms at any time, but obviously most discussions do not lead to transactions.

We expect to expand within other asset classes and geographies through additional acquisitions and future planned organic growth by providing additional specialized investment vehicles within our existing investment asset class solutions. As of the date of this prospectus, we are pursuing additional acquisitions and are in discussions with certain target companies, however the Company does not currently have any agreements or commitments with respect to any acquisitions.”

From the 2021 S-1

P10 IPO

In October 2021, P10 up listed from trading as PIOE on the OTC market to PX on the NYSE through an IPO with lead book running managers Morgan Stanley, JP Morgan, and Barclays. The company sold 23 million class A shares at $12 in the IPO. The shares were half primary and half from insiders. The 130 million raised in funds from the primary sales were directed to corporate debt reductions while the corresponding insider sales reduced insider holdings by approximately 7%. After the IPO, insiders own 57% of the economic interests and 69% of the voting power.

Commencing with the IPO, the previously held 126 million shares of PIOE were reduced to 7 shares for every 10 in a reverse split and became 97 million class B shares with 10x voting rights. Holders of Class B common stock may elect to convert shares of Class B common stock on a one-for-one basis into Class A common stock at any time. With limited exception, upon any transfer, Class B common stock converts automatically on a one-for-one basis to shares of Class A common stock. The voting rights are subject to a “Sunset” provision triggered by when the original class B holders cease to maintain control of 10% of the shares, 25% of the voting rights, or 10 years which ever happens first.

The IPO shares were originally indicated at a $14-$16 range making the final pricing at $12 a disappointment. The unfamiliarity of P10 to market participants was probably the biggest negative factor on the pricing, but the use of dual class stock, even with a sunset provision, likely played a role as well.

As I am investing in P10 specifically for Alpert and Webb’s leadership and vision, I do not see the lack of ability to easily remove them in the first ten years as a negative. I will however miss the price insensitive purchases of PX stock from the index fund buyers of the indexes that do not track dual class stocks. Given the high ownership of PX by insiders already, the use of two class stock seems unnecessary, but my hunch is that Alpert and Webb expect future acquisitions of sizes to be large enough to change the balance of ownership without it.

Value of NOLs

Given the predictability of P10’s earnings stream, P10 is the first NOL shell company I’ve ever owned where I am confident that all federal tax carryover losses will be consumed. The $208mm on 125mm shares is currently worth an undiscounted $1.66 per share in saved taxes.

While we anticipate $0 of federal income tax for several years, we will have some state and local income taxes”

Q3 2021 Investor Presentation

New Credit Line

“A new credit facility provides for a term loan in the amount of $125 million and a revolving commitment in the amount of $125 million. The company will use the loan proceeds to pay off the outstanding borrowings under its existing credit facility, pay off seller’s notes related to the RCP acquisition, and pay transaction-related expenses, as well as for working capital and other general corporate purposes.

Terms of the new credit facility call for a variable interest rate of approximately two and a quarter percent (2.25%) which offers significant savings over the seven percent (7%) interest rate with the previous credit agreement.“

December 23, 2021 announcement

Not only will this net savings of over 5 million annually (4.75% *125mm), the granting of these terms by JP Morgan Chase confirms the stability and visibility of earnings provided by the P10 business model.

Comparables

Hamilton Lane (HLNE, MCap=3.2B, EV=3.7B) with 3x the fee-paying AUM (FPAUM) of P10 and StepStone Group (STEP, MCap =1.9B, EV=3.0B) with 4x are the closest comparable public companies to P10. Both competitors maintain ownership of the performance carry in their funds which increases profitably in rising markets but reduces revenue visibility and steadiness. Both are highly profitable companies with EBITDA margins in the upper 40’s. Unlike P10, STEP provides infrastructure and real estate options.

Hamilton Lane and StepStone both benefitting from growth in private market assets.

Reasons to sell

- If Alpert/Webb were to leave or sell out, I would exit as this is fundamentally a relationship business and the loss of current leadership would likely result in a period of underperformance.

- A more likely risk is that more firms begin to pursue small private alternative asset credit funds and in doing so, increase the cost of P10’s acquisitions.

- If a P10 component fund starts underperforming, its future fundraising will be impaired. This is partially mitigated by P10 continually acquiring new managers with strong histories to increase the number of top performing funds for clients to choose from and keeping product offerings fresh. However, a rash of underperformance not tied to macro events would be a flag.

- Lastly, a major economic change could clearly impact P10 as the alternative asset classes have certainly benefitted from investors seeking substitutes for low yielding securities.

P10 Financials Pre-IPO

Post IPO adjustments

Cash raised from sell of new shares = 130 mm

Post IPO, Debt – Cash = 315.5 + 199 – 21.6 -130 = 362.9 mm

New Share Count (diluted) = 125 mm

Share Price = 11.8 on Jan 30, 2022

Market Cap = 1.475 b

Enterprise Value = 1.84 b

2022 EBITDA est. = 100 mm

2022 EV/EBITDA = 18.4

Valuation

I am using a simplistic model with simplistic assumptions to generate a range of outcomes.

- Organic growth of 15-20%. 2021 organic growth was 30%, but 2021 was a peak cycle year at RCP. 2022 is a low cycle year with fewer new funds scheduled to open than in 2021 or are projected to open in 2023.

- P10 acquisition growth was over 80% in 2021 and I certainly expect more acquisitions in the coming years but modeling more than 10-20% annually seems like magical thinking.

- I expect most acquisitions going forward to be paid with cash from the new credit line, but some transactions may still use a modest amount of common stock. For comparison, the Enhanced acquisition consumed $27 million in stock, while True Bridge required $84 million. Whereas the most recent acquisitions from abrdn were all cash. In the table below, I retain all earnings and increase debt and stock in both scenarios for acquisition funding. More time spent on the cost of acquisitions would improve the model, but a rough guess is sufficient for my purposes.

- I expect a slight increase in the adjusted EBITDA margin as the company scales in FPAUM.

- As organic growth continues, I expect P10 to rate a slightly higher valuation rating closer to HLNE.

The decision to purchase P10 comes down to whether one believes the company can continue to grow AUM at 25% – 40% annually over the next decade through a combination of organic growth and continued accretive acquisitions.

My answer is yes, because I find the P10 business model advantaged in its ability to acquire well-run private asset firms in the attractive alternative asset space at private company prices, incent the management to manage existing assets while continuing to add new ones, and receive a premium valuation for the growth potential.

$PX $100 Baby.

LikeLike

There is certainly a lot of execution required to make that target happen, but the setup, runway, and management is in place for good things to happen.

LikeLike

Good analysis, deep dive, thx.

Any thoughts on Tetragon, British financial conglomerate, strong in asset management and private equity?

Quite some similarities, more mature, but still growing, and a lot cheaper than P10

LikeLike

Haven’t looked at Tetragon in years, but when I did it had a stiff performance fee with no high water mark, so mgmt gets to double dip on collecting its fees after every decline. I believe this explains its discount to NAV.

LikeLike

Great thoughts, thanks for sharing. A few things I was hoping you could shed some light on:

1) I don’t have a good view on is they target 55-60% EBITDA margins, what factors swing that given it’s not very seasonal and recurring? And have they ever said if our AUM reaches a certain threshold we go to 60+% on a more permanent basis?

2) 2 hi-level thoughts – 1) potential concern for PE/alts is if so much capital wants/needs to go into alternatives and so many asset mgrs want more capital to manage, could that create pricing pressure and alts lower fees to attract capital? 2) as a smaller firm, to attract new talent to facilitate deploying larger AUM, do they need to pay much more to get the ppl and cause lower EBITDA margins?

3) also: 1) the niche/target for PX may have enduring tailwinds b/c why would a KKR/BAM/BX want to target PX smaller markets? For the bigs to be successful here would be too tiny to move the needle. And 2) if PX is only investing less than 1% of opportunities that come across the desk, surely they can invest into 2-3% of those and still generate good IRRs for clients. So this means they could productively deploy much more capital/AUM. Curious your take on this or any of the above.

LikeLike

1) There is still a little variability in the revenues and expenses as not every strategy launches subsequent funds on the same calendar cycle, but once the fund is raised the fixed revenue is stable. From what they’ve said, they do see some margin expansion, but they’ve kept it modest (but in the right direction!) The company has dealt with a number of acquisitions and IPO costs this past year. I also expect future m&a and back office costs to decline over time as a percentage of the business as the company scales up an financing costs are also decreasing with the new loan agreement. But yeah, I don’t think we are too far from steady state.

2) Yes, I tend to agree. I do expect more competition. It’s also why I like P10, as the smallest diversified public company in this space, they can still focus on the smaller markets for the foreseeable future and still move the needle. Large players can’t. As for talent remuneration, the managers are getting the full performance carry as assets grow, so will their remuneration grow if they perform. I especially like the incentive that collecting the carry provides to discourage jumping ship as well.

3) Agree on all points. I would add that a macro event or Fed action ending easy money policies would seem to negatively impact some alt sectors, but yet could also create new opportunities. With a contractually guaranteed revenue stream and a highly manageable debt load, P10 is well positioned to adapt as necessary.

LikeLike